1. Vanishing Grid Quotas: The High Cost of “Occupying without Generating”

Many European solar projects built between 2010 and 2016 represented the technology level of their time. A decade later, however, these systems are revealing a structural problem.

They often occupy strong grid connection points, good rooftops or well-located land. But many of them were built with lower-power modules, older system designs and early-generation component technologies. After years of operation, additional issues may appear: module degradation, inverter aging, hotspot risk, cable losses and lower system availability.

The result is a form of grid underutilization: valuable connection capacity remains occupied, but the site does not generate the level of electricity value that its location and grid position could support.

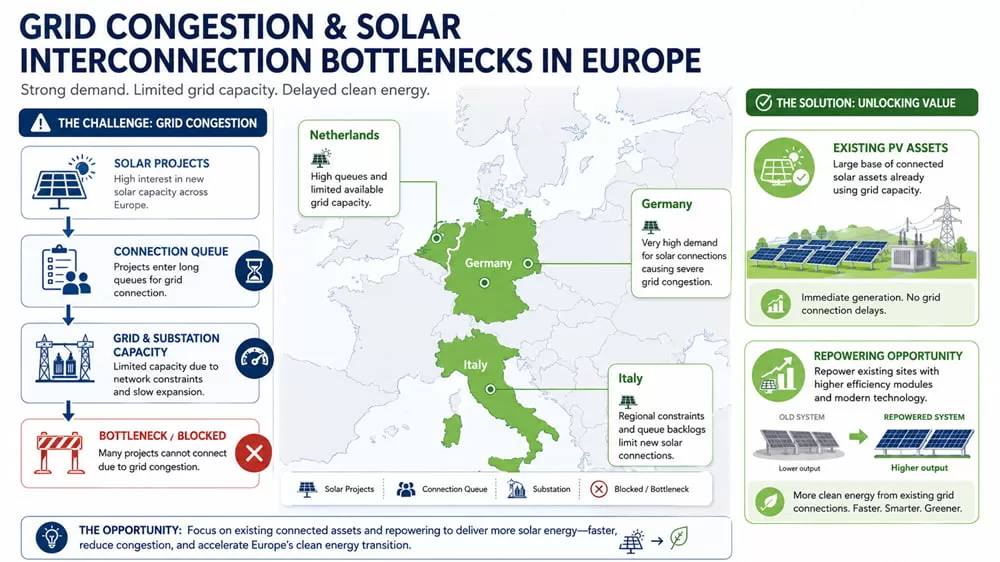

This problem becomes more serious as grid congestion intensifies across Europe. In the Netherlands, RVO explains that grid congestion can lead both new and existing users to be placed on waiting lists for additional transport capacity or upgraded connections. RVO also states that, from 1 July 2026, small-scale users that have not been given priority will also be placed on waiting lists in congested areas. (RVO.nl)

Italy shows a similar pressure point. According to Terna’s 2025 Development Plan, renewable energy connection requests reached 348 GW by the end of 2024, including 152 GW of solar projects. This demonstrates that Europe does not lack project ambition; in many markets, it lacks available, usable and timely grid space. (Terna)

In this environment, every square metre of an underperforming rooftop becomes a financial leak.

It can mean:

lower annual yield;

weaker return per square metre;

reduced asset valuation;

lower financing attractiveness;

higher opportunity cost;

inefficient use of scarce grid capacity.

When grid access becomes scarce, low-efficiency operation is no longer just a technical issue. It becomes an asset management problem.

3. Module Selection: Why the 2026 “Space Race” Leaves No Room for Cheap Components

Module selection in a repowering project is fundamentally different from module selection in a new-build project.

In a greenfield project, a developer may sometimes compensate for lower module efficiency by expanding land use. In repowering, that flexibility is often limited.

The project is already constrained by:

roof area;

land boundaries;

existing mounting layout;

structural load limits;

inverter configuration;

cable routes;

grid connection capacity.

This means repowering is a space-efficiency game.

Within a fixed footprint, the modules that can deliver higher usable power, lower degradation and stronger long-term performance will unlock greater asset value.

For this reason, comparing only the module price per watt can be misleading. In repowering, the real financial variables are:

power density;

reliability;

degradation rate;

temperature behaviour;

structural compatibility;

lifetime energy yield;

long-term LCOE.

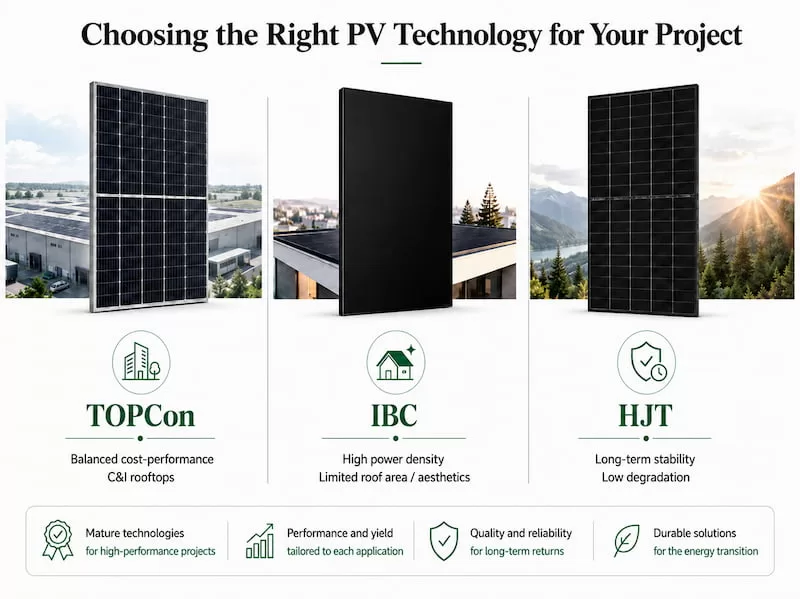

3.1 TOPCon: The Standardized Upgrade Path for Most C&I Rooftops

TOPCon is well suited for a large share of commercial and industrial repowering projects, especially warehouses, factories, logistics buildings and large flat rooftops.

Its strength lies in the balance between efficiency, cost, supply maturity and system compatibility. For many legacy C&I rooftops still operating with older P-type modules, TOPCon can provide a practical upgrade path: higher power density without pushing project budgets too far outside mainstream expectations.

Typical applications include:

warehouse rooftops;

factory rooftops;

commercial buildings;

cost-sensitive C&I assets;

large-scale rooftop portfolio upgrades.

For EPCs, the value of TOPCon is scalability. It can serve as a repeatable, standardized solution for a broad range of repowering projects.

3.2 IBC: High-Value Density for Restricted and Premium Rooftops

IBC is especially relevant for rooftops where available space is limited, structural load must be carefully managed, or visual appearance matters.

Typical applications include:

premium commercial buildings;

office rooftops;

residential or mixed-use buildings;

limited-area C&I rooftops;

projects with aesthetic requirements;

sites where roof leasing costs make every square metre economically valuable.

The value of IBC is not simply that it is a higher-efficiency technology. Its value lies in improving revenue density per square metre.

For older buildings, roof space and structural capacity are often the main constraints. By using modules with higher power density, owners can increase system output without significantly increasing the project footprint or structural load.

This is where the IBC premium becomes easier to explain:

You are not only buying a more advanced module. You are buying higher revenue density from a limited rooftop asset.

3.3 HJT: Stability for Southern European and Long-Term Assets

HJT is particularly suitable for high-irradiance, high-temperature and long-term operating environments, especially in Southern Europe and older ground-mounted plants.

In markets such as Spain, Southern Italy and Greece, long-term performance is not determined only by nameplate power. It also depends on how the module behaves under heat, irradiance stress and long operating hours.

HJT’s lower degradation potential and stronger temperature behaviour can support more predictable long-term yield, making it attractive for owners focused on 25-year cash-flow stability.

Typical applications include:

Southern European high-temperature regions;

aging ground-mounted plants;

long-term ownership assets;

investors focused on yield stability;

projects sensitive to degradation and heat-related losses.

For owners who care less about short-term CAPEX and more about long-term cash flow, asset stability and financing credibility, HJT can be a strong technology option.