The European solar market has not slowed in 2026, yet the decision-making logic of companies is evolving. As incentive mechanisms are adjusted, grid connection rules tighten, grid capacity constraints increase and solar panel price trends fluctuate, the market environment is shifting from scale expansion towards structural balance.

With revenue mechanisms becoming increasingly market-driven and policy certainty declining, the solar panel is no longer merely a cost component. Instead, it has become a key variable influencing power generation performance and long-term system stability. In this changing investment environment, re-evaluating solar panel selection has become an inevitable step for many companies.

Table of Contents

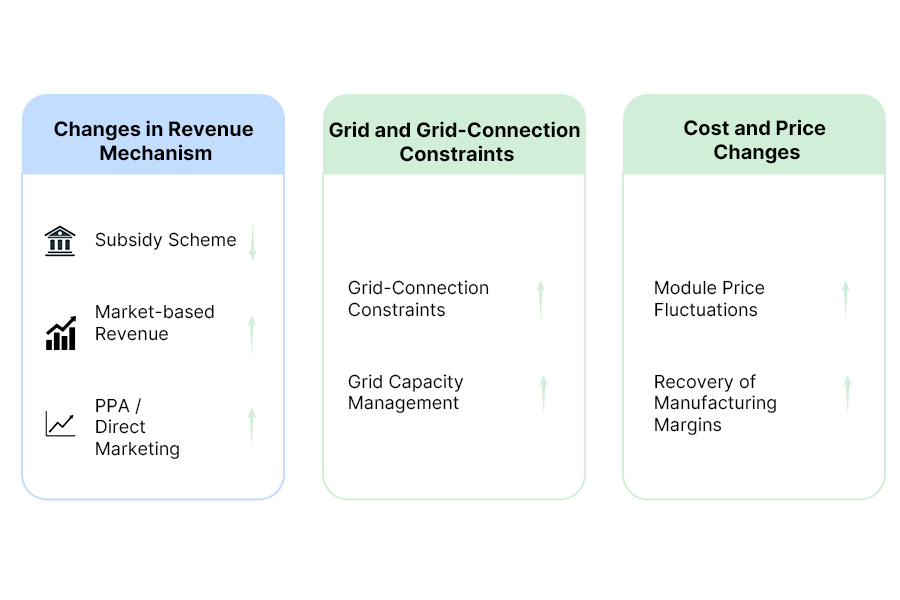

Three Structural Changes in the European Solar Policy Environment in 2026

The European solar market continues to grow in 2026, but the framework supporting the market is changing. The investment environment is gradually shifting from a relatively stable policy-driven model to a phase where market mechanisms and structural constraints coexist.

Recent policy measures introduced or discussed across several key markets point in a similar direction: revenue structures are becoming more dependent on market signals, grid connection capacity management is becoming more refined, and the importance of compliance and risk control is increasing. These developments do not represent isolated national adjustments, but rather a structural rebalancing of the European energy system as renewable penetration continues to rise.

Against this backdrop, three long-term policy shifts can be observed.

1.1 Revenue Mechanisms Are Gradually Becoming Market-Oriented

Several European countries are adjusting traditional subsidy frameworks.

In Germany, the draft amendment to the Renewable Energy Act (EEG) proposed in 2026 signals a reassessment of fixed subsidy models. The proposal includes the gradual removal of fixed subsidies for small private solar systems and stronger reliance on direct marketing mechanisms. This means that more solar installations will increasingly be exposed to wholesale electricity price fluctuations.

In France, discussions around the evolving PPA market structure and the rebalancing of the national energy plan (PPE3) reflect a stronger reliance on market-based electricity trading.

In Italy, incentive schemes are becoming more tightly linked to compliance conditions. Violations may lead to incentive reductions of 10%–50%, accompanied by stricter regulatory supervision and auditing.

These changes do not imply the disappearance of subsidies. Rather, they indicate that the stability of project revenues will no longer be fully guaranteed by policy, but will depend increasingly on the actual power generation capability and long-term performance of the solar system.

In this context, parameters such as the temperature coefficient, degradation curve, authenticity of bifacial gain, and low-irradiance performance of solar panels are increasingly entering financial modelling. Power generation differences that could previously be offset by subsidies must now be supported by the technical performance of the solar panels themselves.

1.2 Grid Capacity and Connection Mechanisms Are Becoming Core Variables

Italy’s 2026 grid reform under the Bollette Decree introduces project maturity as a key screening criterion. Grid capacity is dynamically allocated through the Terna portal and a “micro-zone” management system, with connection solutions competing within designated application windows. This mechanism changes the traditional first-come, first-served approach and effectively turns grid capacity into a competitive resource.

In Germany, uncertainty surrounding the AgNes grid tariff reform and the potential removal of storage grid fee exemptions has already delayed investment decisions in large battery and solar-plus-storage projects.

France’s energy planning also highlights grid capacity allocation and system balance, particularly in the context of large-scale solar plants and adjustments to the country’s nuclear energy structure.

These developments send a clear signal: grid connection capability and system compatibility are becoming decisive factors in project feasibility.

Under such conditions, evaluating solar panels is no longer limited to comparing watt-level efficiency. Instead, several additional factors must be considered:

-

compatibility between current levels and inverter specifications

-

alignment between panel size and rooftop structural capacity

-

the impact of glass-glass versus glass-backsheet structures on weight and installation efficiency

-

stability of the power generation curve under curtailment or flexible grid-access mechanisms

As a result, system compatibility in solar panel selection is becoming significantly more important.

1.3 Changing Cost Expectations and Price Dynamics

At the beginning of 2026, solar panel prices in the European market experienced a temporary rebound. Although upstream wafer prices have recently declined, manufacturers have begun restoring profit margins after a prolonged period of losses. As a result, prices for some solar panel products have risen by approximately 15–18% from the lows recorded in 2024.

At the same time, geopolitical uncertainty and changes in the trade environment are increasing market volatility, meaning that future price trends may no longer follow a clearly downward trajectory.

This development challenges assumptions formed in recent years. Solar panel prices may not continue to decline indefinitely, and strategies based solely on waiting for lower procurement costs are becoming less predictable.

Against a backdrop of price fluctuations and policy restructuring, companies are starting to reassess the role of cost per watt in investment decisions. Greater attention is now being directed towards long-term power generation stability, technological maturity, and the compatibility between different solar panel technologies.

How Policy Changes Are Reshaping the Value Criteria for Solar Panels

Adjustments to policy mechanisms and changing price expectations are significantly altering the criteria used in solar panel selection. Beyond procurement cost, factors such as power generation stability, structural compatibility and long-term reliability are increasingly becoming core evaluation elements.

2.1 From Cost per Watt to Long-Term Power Generation Performance

As subsidy certainty declines, the predictability of power generation performance has become a key variable. Parameters such as temperature coefficient, annual degradation curve, the authenticity of bifacial gain and performance under low-irradiance conditions are increasingly incorporated into revenue modelling and project financing assessments.

Within this framework, different solar panel technologies occupy distinct positions:

-

TOPCon solar panels maintain a balanced combination of efficiency, cost and supply maturity. They remain the mainstream choice in Europe’s commercial and industrial solar market, particularly for projects sensitive to payback periods and procurement availability.

-

HJT solar panels typically feature a superior temperature coefficient (around -0.243%/°C) and a lower degradation trajectory. Their advantages in long-term generation stability are more evident in high-temperature environments or projects designed for long-term asset ownership.

-

IBC solar panels often provide higher front-side efficiency potential in premium distributed rooftop applications. Their strengths are mainly reflected in value per square metre and rooftop adaptability.

Panel structure is also increasingly influencing project revenue assessments. Double glass solar panels offer advantages in long-term durability and weather resistance, while glass-backsheet panels provide greater flexibility in terms of weight and installation efficiency. Bifacial solar panels can deliver additional gains in high-reflectivity environments, although the actual yield must be evaluated according to installation conditions.

As a result, technology selection is gradually shifting from simple efficiency comparisons towards scenario matching and long-term performance evaluation.

Comparison of TOPCon, HJT and IBC Solar Panel Technologies

| Technology | Structure | Key Performance | Typical Applications |

|---|---|---|---|

| TOPCon | N-type tunnel oxide passivated contact structure | Temperature coefficient about −0.32%/°C; balanced efficiency and cost with mature mass production | Commercial & industrial rooftops and large solar plants focused on stable ROI |

| HJT | Heterojunction structure with strong bifacial generation capability | Temperature coefficient about −0.243%/°C; bifaciality typically 90–95% | High-irradiation regions, agrivoltaics and solar carports where bifacial gain is effective |

| IBC | Back-contact design with no front grid lines | Temperature coefficient about −0.29%/°C; clean appearance and better shading tolerance | BIPV and premium residential or commercial rooftops requiring strong aesthetics |

Note: Parameters and application descriptions reflect common industry references. Actual performance may vary depending on specific solar panel models and testing conditions.

2.2 From Maximum Power to System Compatibility

Stricter grid connection rules, current limitations and inverter compatibility constraints are making the coordination between solar panel parameters and system design increasingly important. Higher wattage panels do not necessarily represent a better configuration. Current design, voltage ranges and inverter compatibility have become key considerations.

For example, solar panels using 1/3 cut cell designs or optimised current structures can reduce series current losses while improving operational stability. In commercial and industrial rooftop projects where structural load capacity is limited or approval requirements are strict, panel dimensions and weight also influence installation risks and structural assessment outcomes.

Under these conditions, balancing power density, current control and structural design is often more meaningful than pursuing higher nominal panel power alone.

2.3 From Parameter Comparison to a Risk Management Framework

Increasing uncertainty in both policy and market conditions is prompting financial institutions and project developers to place greater emphasis on technology maturity and bankability. Certification systems, production stability, long-term supply capability and product consistency are becoming implicit evaluation indicators.

Mainstream solar panel technologies benefit from mature supply chains and well-established standards, giving them advantages in financing and risk control. By contrast, structural innovations—such as full-black panels, transparent backsheet designs or specialised aesthetic configurations—tend to serve specific application scenarios rather than representing universal replacement solutions.

Within this evolving framework, solar panel selection is gradually becoming part of broader risk management decisions, rather than simply a comparison of technical parameters.

Three Key Criteria for Solar Panel Selection in Europe in 2026

In the European market in 2026, solar panel selection is increasingly based on practical constraints and revenue structures rather than purely on parameter comparisons or nominal power levels. Considering the policy and market shifts discussed earlier, three core evaluation dimensions can be identified.

Criterion 1: Is the Revenue Structure Fully Market-Oriented?

When projects rely on PPAs, direct marketing or floating electricity prices, the stability of power generation performance becomes directly embedded in cash-flow forecasting models. In this context, factors such as the temperature coefficient and degradation trajectory of solar panels are no longer just technical specifications but key variables affecting revenue stability.

Therefore, in projects with highly market-driven revenue models:

-

If the objective is to control long-term degradation and fluctuations in the generation curve, technologies with lower degradation paths and stronger temperature performance become more advantageous. For example, solar panels using highly stable cell structures and glass-glass encapsulation often deliver more consistent output under long-term operation and high-temperature conditions.

-

If a project focuses more on payback periods and early-stage cash flow balance, mainstream technologies that maintain a strong balance between efficiency and cost are often more practical. In Europe, N-type TOPCon solar panels currently represent one of the most widely deployed solutions, combining efficiency, pricing and manufacturing maturity.

-

In projects with favourable ground reflectivity conditions, bifacial solar panels can more effectively capture rear-side gains. In scenarios where space functionality is also important—such as solar fencing, agrivoltaics or semi-transparent canopies—transparent glass-glass panels may offer greater value. Actual gains, however, must be assessed based on installation height, reflectivity, transparency levels and array layout rather than theoretical bifaciality alone.

-

In premium building-integrated or architecture-sensitive projects, grid-free front designs or full-black solar panels may offer stronger visual compatibility, although trade-offs between efficiency and cost must still be considered.

Under these conditions, the ranking of technologies becomes increasingly tied to project revenue structures, rather than being determined purely by efficiency comparisons.

Criterion 2: Does the Grid Create Structural Constraints?

Where grid connection capacity is limited, current restrictions are defined or inverter compatibility requirements become stricter, the system-level coordination of solar panels becomes a critical factor.

When string current limits apply, optimised current designs or advanced cell segmentation structures can reduce series losses and improve operational stability. In commercial and industrial rooftop projects with limited structural load capacity, panel size and weight can directly affect structural approval processes and installation risk. In markets where grid-access windows are highly competitive, higher power density per square metre may also help optimise layout within limited capacity allocations.

Under such conditions, increasing the nominal power of a single solar panel is not always the optimal strategy. Instead, factors such as current control, structural weight, panel dimensions and inverter compatibility ranges often become more decisive than maximum panel wattage.

Criterion 3: Is the Financing and Risk Environment Becoming More Conservative?

Amid policy adjustments and uncertain price expectations, banks and investors are placing greater emphasis on technology maturity and standardisation. Production scale, certification frameworks, long-term supply stability and supply chain completeness are becoming implicit factors influencing financing conditions.

For projects that depend on bank financing or asset securitisation, mainstream solar panel technologies with large installed bases and mature supply chains are generally more likely to gain acceptance from financial institutions. By contrast, for self-owned projects or specialised applications—such as architecture-sensitive BIPV installations—structural innovations and customised panel designs may provide differentiated value rather than serving as universal replacements.

In an environment of declining risk tolerance, solar panel selection is gradually becoming part of broader risk management strategies, rather than simply a decision about adopting new technologies.

In a European market where policy structures continue to evolve, solar panels are no longer merely hardware components. They are becoming integral elements within revenue models and risk management frameworks. Companies are reassessing their solar panel selection criteria not because of technological updates alone, but due to shifts in investment logic and risk structures.

These changes may not always be immediately visible, but they are already reshaping technology rankings and competitive dynamics. In the future, competition between solar panels will not depend solely on efficiency and price, but increasingly on stability, system compatibility and long-term predictability.

Maysun Solar supplies IBC solar panels, TOPCon solar panels and HJT solar panels for the European market, focusing on aligning technology with specific project conditions. Key factors include temperature performance, degradation behaviour, current design and panel structure, helping partners select suitable solar panel solutions that ensure stable and predictable system performance.

Reference

pv magazine Deutschland. EEG-Entwurf geleakt: komplette Streichung der Förderung privater Photovoltaik-Anlagen vorgesehen. 26 February 2026.

https://www.pv-magazine.de/2026/02/26/eeg-entwurf-geleakt-komplette-streichung-der-foerderung-privater-photovoltaik-anlagen-vorgesehen/

pv magazine Deutschland. Investitionssicherheit akut gefährdet: Netzentgeltreform für Großbatteriespeicher. 26 February 2026.

https://www.pv-magazine.de/2026/02/26/investitionssicherheit-akut-gefaehrdet-netzentgeltreform-fuer-grossbatteriespeicher/

pv magazine Italia. Incentivi fotovoltaico 2026 e controlli GSE: cosa cambia con il nuovo regolamento. 26 February 2026.

https://www.pv-magazine.it/2026/02/26/incentivi-fotovoltaico-2026-e-controlli-gse-cosa-cambia-con-il-nuovo-regolamento/

pv magazine Italia. DL Bollette: decongestione delle reti, alcune riflessioni. 25 February 2026.

https://www.pv-magazine.it/2026/02/25/dl-bollette-decongestione-delle-reti-alcune-riflessioni/

pv magazine France. Comprendre et anticiper les mutations du marché des PPAs en France. 27 February 2026.

https://www.pv-magazine.fr/2026/02/27/comprendre-et-anticiper-les-mutations-du-marche-des-ppas-en-france/

pv magazine France. Les prix des modules solaires augmentent plus rapidement que prévu en février. 26 February 2026.

https://www.pv-magazine.fr/2026/02/26/les-prix-des-modules-solaires-augmentent-plus-rapidement-que-prevu-en-fevrier/

SolarPower Europe. EU Solar Market Report 2025–2026.

https://www.solarpowereurope.org/eu-solar-market-report

Recommend reading

How to Choose Solar Panels for Low-Load-Bearing Industrial Roofs: A Guide to Weight, Power Density and Mounting Systems

Choosing solar panels for a low-load-bearing industrial roof requires more than checking the weight of an individual module. A more reliable process starts by determining the roof’s remaining load-bearing capacity. The complete load from the modules, rails, fasteners and ballast must then be

Why Do Solar Panels Lose Power in Hot Weather? How Temperature Coefficient and Roof Ventilation Affect Summer Energy Yield

Summer brings stronger sunlight and longer daylight hours, so it is normally one of the most productive seasons for a solar system. However, some system owners notice that solar panel output does not continue to rise during the hottest part of the day.

How to Design a Low-Maintenance Rooftop Solar System

Introduction A low-maintenance rooftop solar system is not created after installation. It is designed before installation. Over a 20–30 year operating life, rising O&M costs are rarely caused by dirty glass alone. They are more often caused by design decisions made at the

European Heatwaves and PV Self-Consumption: Why HJT Solar Modules Perform Better in Hot Summers

Across Europe, summer heatwaves are no longer just a climate or comfort issue. They are becoming an energy-use issue. During hot summer days, air conditioning, ventilation, refrigeration, office equipment and industrial cooling loads can rise exactly when rooftop solar modules are exposed to

Partial Shading on Solar Panels: Why a Small Shadow Can Cause Major Power Losses

Introduction: Shading Is Not Just a Surface Area Problem In a photovoltaic system, a small shadow can be amplified by the electrical structure of the module. In a typical module with three electrical sections, a shaded area covering only a small part of

From Half-Cell to Multi-Cut: Why PV Modules Are Paying More Attention to More Segmented Circuit Design?

Table of Contents In recent years, half-cell modules have become a mainstream design in the photovoltaic market. Compared with traditional full-cell modules, half-cell technology reduces the operating current of each cell unit, lowers internal resistive losses, and improves thermal management and partial shading